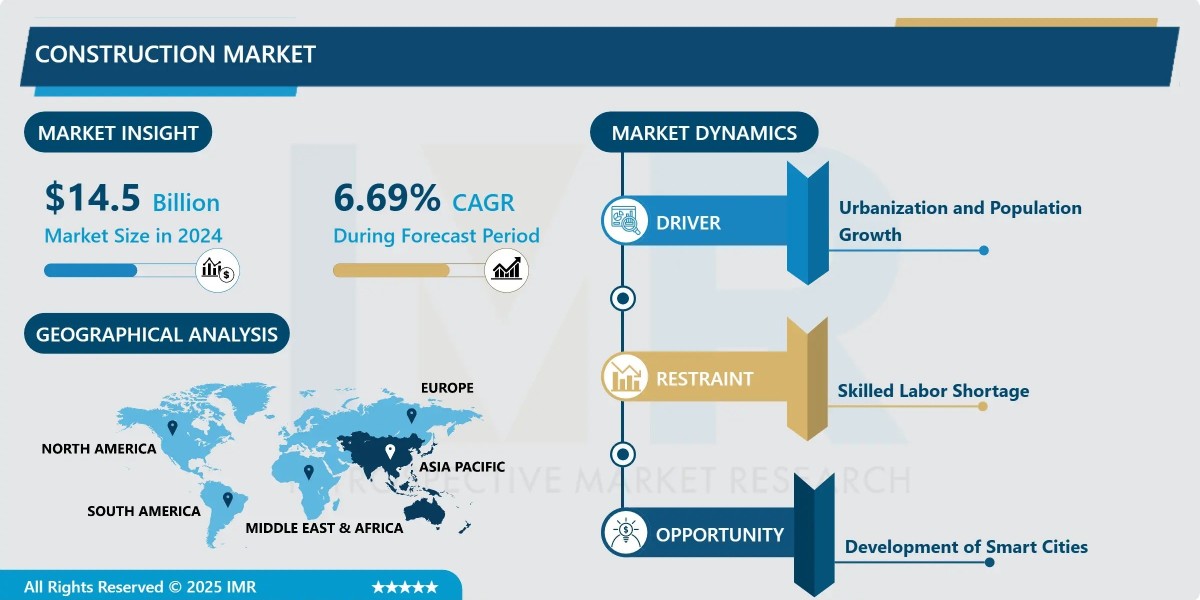

According to a new report published by Introspective Market Research, Construction Market by Sector, Construction Type, Service, and Region, The Global Construction Market Was Valued at USD 14.5 Trillion in 2024 and is Projected to Reach USD 24.34 Trillion by 2032, Growing at a CAGR of 6.69%.

Market Overview:

The global Construction market is a vast and multifaceted industry encompassing the planning, design, financing, building, and maintenance of physical structures and infrastructure. This market includes residential, commercial, industrial, and civil (infrastructure) construction activities. Modern construction offers significant advantages over traditional methods through technological integration: Building Information Modeling (BIM) enables precise digital planning and collaboration, modular and prefabricated construction enhances speed and reduces waste, and advanced materials improve durability and sustainability. These innovations lead to more efficient project delivery, cost control, and the creation of smarter, more resilient built environments.

Growth Driver:

The paramount growth driver for the global construction market is the unprecedented wave of urbanization and the corresponding need for massive infrastructure development and housing, particularly in emerging economies. As populations rapidly migrate to cities, governments and private developers are compelled to invest trillions in constructing new residential complexes, commercial hubs, transportation networks (roads, railways, airports), and utilities (water, power). This is compounded by national strategic initiatives like China's Belt and Road, India's National Infrastructure Pipeline, and the U.S. Infrastructure Investment and Jobs Act, which allocate historic levels of funding to modernize and expand physical infrastructure. This dual demand for both social infrastructure (housing) and economic infrastructure (transport, energy) creates a sustained, multi-decade growth cycle for the construction industry worldwide.

Market Opportunity:

A transformative market opportunity lies in the widespread adoption of sustainable construction practices, digital transformation, and off-site modular construction. The global push for net-zero carbon emissions is driving demand for green buildings, energy-efficient retrofits, and the use of low-carbon materials. Simultaneously, the digitalization of the sector through BIM, IoT (Internet of Things) for smart job sites, drones, and AI-powered project management software offers immense potential to boost productivity, safety, and profitability. Furthermore, the modular and prefabricated construction segment presents a high-growth avenue to address skilled labor shortages, reduce construction timelines, minimize environmental impact, and improve quality control, especially in the residential and institutional building sectors.

Construction Market, Segmentation

The Construction Market is segmented on the basis of Sector, Construction Type, and Service.

Sector

The Sector segment is further classified into Residential, Commercial, Industrial, and Infrastructure. Among these, the Infrastructure sector accounted for the highest market share in 2024. The infrastructure segment, encompassing transportation (roads, bridges, railways), energy & utilities, and other public works, dominates due to colossal government and public-private partnership (PPP) investments. These large-scale, capital-intensive projects are critical for economic competitiveness and societal function, driving the highest value of construction output globally, particularly in developing regions undergoing rapid modernization.

Construction Type

The Construction Type segment is further classified into New Construction and Renovation & Maintenance. Among these, the New Construction sub-segment accounted for the highest market share in 2024. New construction leads the market, fueled by greenfield projects in expanding urban areas, the development of new industrial parks, and the creation of new transportation corridors. The demand to build new assets to support economic growth and population expansion in Asia-Pacific, the Middle East, and Africa significantly outweighs renovation spending in volume, making it the larger segment.

Some of The Leading/Active Market Players Are-

- China State Construction Engineering Corp., Ltd. (CSCEC) (China)

• Vinci SA (France)

• ACS Actividades de Construcción y Servicios, S.A. (Spain)

• Bouygues S.A. (France)

• Hochtief AG (Germany)

• Skanska AB (Sweden)

• Larsen & Toubro Ltd. (India)

• Bechtel Corporation (USA)

• Fluor Corporation (USA)

• AECOM (USA)

• Balfour Beatty plc (UK)

• STRABAG SE (Austria)

• Obayashi Corporation (Japan)

• Shimizu Corporation (Japan)

• Kajima Corporation (Japan)

• and other active players.

Key Industry Developments

News 1:

In March 2024, Vinci, through its subsidiary Eurovia, secured a €2.5 billion contract to design and build a major high-speed rail section in Europe, highlighting the sustained mega-project momentum in the infrastructure sector and the role of large conglomerates in delivering complex projects.

News 2:

In February 2024, Skanska announced a strategic partnership with a proptech firm to deploy an AI-powered platform across all its Nordic construction sites. The system uses sensors and analytics to optimize logistics, monitor safety compliance in real-time, and predict project delays, showcasing the industry's move towards data-driven construction.

Key Findings of the Study

- The Infrastructure sector dominates, driven by massive global investments in transportation and energy projects.

• The Asia-Pacific region is the largest and fastest-growing market, fueled by urbanization and government spending.

• Rapid global urbanization and corresponding massive infrastructure and housing needs are the key growth drivers.

• Major trends include the acceleration of sustainable/green building, digitalization (BIM, AI, IoT), and the adoption of modular construction methods.